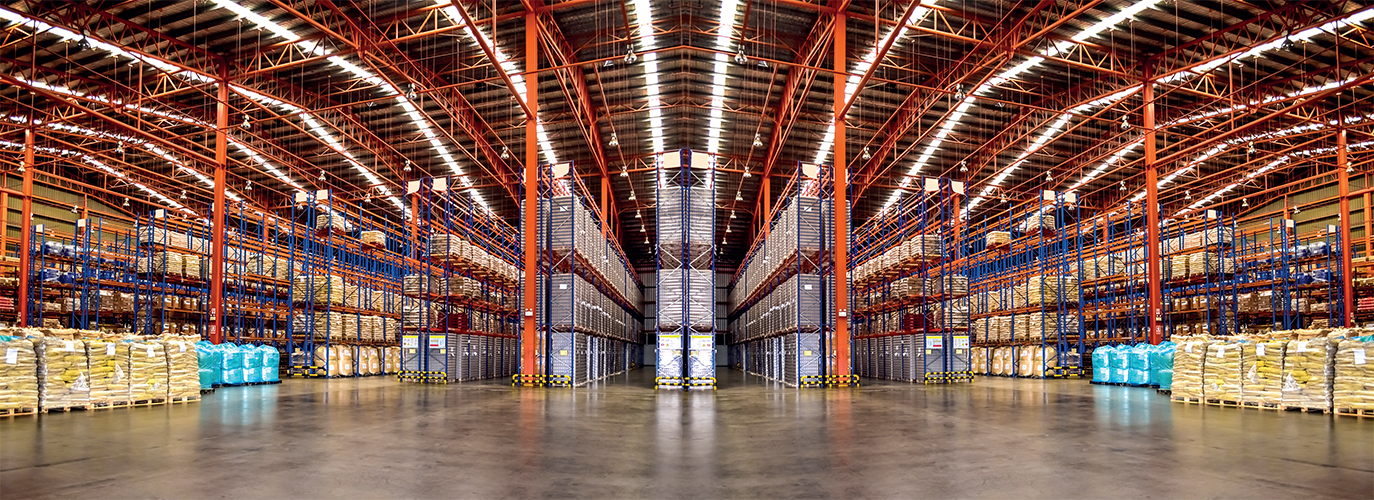

Supply and demand

Over the course of the last 24 months, the stories around the medical fallout related to Covid-19 have only been equaled perhaps by the number of articles discussing the serious impact that has been recognized in the supply chain. Specifically challenges in global sourcing and bringing goods to market have caused delays and shortages for products, as well as raised prices for consumers. Due to the Covid-19 pandemic, consumers have shifted more of their purchases online, which has caused tremendous demands on fulfillment warehouses to operate as efficiently as possible to get products to their customers on time and on budget. But there simply are not enough industrial fulfillment centers across the country to support this sudden spike in online retail, thus spurning an investment and development push for the construction of more e-commerce specific industrial facilities, both large and small. We are still in the advent of the e-commerce revolution, so the trends we are experiencing now are only the beginning of a fundamental shift on how we buy the goods and services we need. But to fulfill these consumer demands,we will be required to build more industrial infrastructure in both 2022 and beyond. Here is a take on the trends for 2022.

- The continued rise of industrial real estate development. Over the last two years as consumers spending has shifted, the need for more industrial real estate space to meet the demands of consumers buying goods online and having them fulfilled through distribution centers has increased. Typically an e-commerce specific fulfillment center requires three times the square footage of a standard B2B distribution center because of the accessibility to a larger variety of SKUs. At the height of the Covid pandemic last year, e-commerce sales represented a mere 15.7 percent of overall retail sales, and have since cooled off to 13.3 percent as more brick-and-mortar stores have reopened. But the trend towards buying more online will only continue and in just three years, it is forecasted that the percentage of retail that is purchased online will nearly double to 26 percent. All of this growth will require the construction of new facilities, with forecasts showing that to support the growth of e-commerce 300 to 400 million-square-feet of industrial development will be needed by 2025.

- The push towards bigger industrial buildings. During the pandemic, e-retailers that had the largest e-commerce platforms and the greatest breadth of products clearly outperformed those that were niche centric. Thus having a larger fulfillment center, where you can consolidate orders and carry a wide range of products provides competitive advantage for e-retailers. Walmart, Amazon, Wayfair, Home Depot and other retailers with a strong online presence recorded record growth on their e-commerce platforms. And despite e-commerce sales representing less than a quarter of overall retail sales in the United States, this number is still anticipated to grow to just over 26 percent by 2025. Yet in China, their forecast is 57 percent of retail sales, so there is still room for growth in the US.

- The push towards smaller last-mile facilities. With transportation costs typically eating up 50 percent or MORE of supply chain costs, being closer to consumers is critical to reduce costs. Thus the model of having only one point of distribution to support North America is dead. The new model is more complex with several larger distribution centers supporting many smaller facilities in regions closer to populations and/or last mile fulfillment centers. Incredible demand has been seen in urban sites that have cross-docking capabilities, especially those that have space to store last-mile vehicles. This has given new life to older facilities that may not be suited for modern distribution, but can still serve a very valuable purpose based on their geographical location close to consumers. More facilities closer to consumers also means faster delivery times to consumers as well as fewer miles driven, which equates to a smaller carbon footprint. Wins for the consumer and the business.

- Industrial construction in new emerging markets are evolving. With transportation costs as the primary driver of overall supply chain costs, coupled with consumer expectations that the speed of e-commerce delivery in New York City should be the same in Amarillo, Texas, drive time and costs to deliver in new emerging consumer markets means that the core industrial markets are not the only place where we will see industrial construction growing. Already, with a large migration of people from the Northeast migrating to the Southeast, particularly Florida, the demand for industrial buildings has grown tremendously, particularly in the I-4 corridor, a central region that can reach most of the state population and back within a day’s drive. Similarly, across the nation new emerging markets are being developed where fulfillment centers in locations that are giving more consumers faster delivery times for their e-commerce orders which means that the secondary, tertiary and emerging markets are all destined to see industrial development to meet the delivery times and costs that consumers expect.

- Increases in both construction time and costs. All of this anticipated growth in industrial development will further exacerbate the already strained building material supplies market. With more than 30 percent of building supplies sourced from China, and the previous aforementioned issues of factory shut downs, reduced work hours and supply chain constriction among all nodes, lead times are increasing – oftentimes tripling in length – causing further delays in construction projects. Many times, it is just one critical part which can hold up the entire project. All of these costs related to scarcity of products and delays in construction are already being passed on to owners as construction costs have increased about five percent this past year, from both labor and materials. That number is expected to further increase in 2022 to play catch up to unforeseen supply issues experienced in 2021.

These are just the impacts related to supply change challenges that will shape the evolution of industrial real estate as well as construction in 2022 and beyond. It will take time to reach an equilibrium where manufacturing supply and demand come to an equilibrium that can be delivered on time and on budget again. Do not expect this balance to be achieved in 2022, so builders (and consumers) can anticipate higher costs for the foreseeable future. Despite these increases in construction time and costs, the demands for e-commerce infrastructure, which needs to be supported by new industrial development will drive growth at a minimum for the next several years.

Gregg Healy is executive vice president and head of Savills Industrial Services Group in North America. Based out of the Orange County, California office, he manages the company’s industrial practice in the US and Canada as a single, unified force – setting strategy and best practices, as well as guiding service delivery and client solutions across markets. In this leadership role, he is committed to matching Savills industrial and logistics advisory capabilities with client needs by continuously refining the company’s industrial market footprint and service platform.

https://www.savills.com/